One way I introduce the topic of the eurozone troubles is to review crises of recent decades. As is usual with currency crises, they compel some pretty heated rhetoric. It’s not surprising. When the currency is mismanaged — badly mismanaged — society suffers. Weimar Germany and Mugabe Zimbabwe are examples. So should be post-WW1 Britain, in my view. True, it suffered no hyperinflation. But the fear of it drove central bankers to the opposite extreme. How can 20% unemployment in defense of currency “stability” be good management? But I digress. The most heated — and vacuous — rhetoric comes in defense of the monetary order. Again, this is usually inspired by genuine concern over what could go wrong, a-la Zimbabwe. So let’s look at some ghosts of crises past and pick out the rhetoric.

Consider John Major, Prime Minister at the time of Britain’s fall from eurodreams grace, otherwise known as Black Wednesday. On September 16, 1992, Britain gave up the project of monetary unification in Europe, by leaving the DM peg known as the Exchange-rate Mechanism (ERM). The cost was too high. Fifteen percent central bank interest rates for what? Currency “stability”. Days before the devaluation, Major warned darkly that “it is a cold world outside the ERM.” Priceless.

(If you thought Anatole Kaletsky is a Johnny-come-lately, the following should set you straight.)

Too much ink has been spilt on the 1997-98 East Asia crisis to warrant further mention. Except to say that this was a defining event in my education. This crisis belonged to the new generation of crises, those catalysed or at least facilitated by convertibility on the capital account — in other words, by freely tradable currencies. The Tequila crisis of 1994 kicked it all off. The Asia crisis brought down even the keenest tiger: Korea.

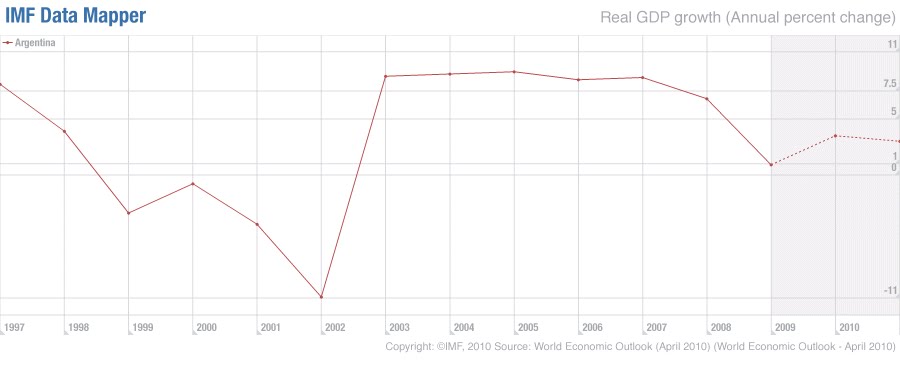

For my money, nothing beats Argentina. As noted, it had much at stake in the currency arrangements known as the Convertibility Plan. Bouts of hyperinflation will do that. And the IMF had a big stake in this race. Argentina was its star reformer. Make no mistake, much good came from this. The country was the first, I believe, to adopt a fully-funded public pension system. And, of course, hyperinflation was vanquished. The only trouble was the near-inevitable incompatibility of fixed currencies with financial globalization. “Near inevitable” because the only way to marry these is to surrender monetary autonomy. And the only way to do that sustainably is to have near-perfect flexibility in domestic prices (mainly wages). And the only way to do that is to be Hong Kong. But that didn’t prevent seas of rhetorical and financial ink from being spilt in avoidance of the inevitable. (Argentina gave up the peg in January 2002.)

Anne Kruger, the Fund’s policy tsar, dispensed the usual requirements dictated in the death throes of an unsustainable (overvalued) currency regime. These remarks accompanied the press release above. See if any of this sounds familiar.

At least there was no talk of an end to civilization or any other “existential threat” to the nation. At least not from the Fund. Undoubtedly there was such rhetoric from people closer to the currency regime. In any case, the currency arrangements are hard to dispose. All manner of fudge is attempted before just accepting the inevitable. I think a sampling of headlines sums up the point.

Wow. Did you catch that last headline? That one really surprised me. If you have an FT or Factiva account, do try to read that article. Keep in mind the peso collapsed just after the euro got started.

Do remember that devaluation for Argentina was bullish. Unambiguously. For Spain and its other creditors, not so much….

Argentina in the New World Order was a darling of the Fund. You can browse its archives to sample the hagiography. IMF MD Michel Camdessus in 1996 could not be more glowing about this star pupil.

This is now my fourth trip to Argentina as Managing Director of the Fund, and each time I come here, I am amazed by how much things have changed since I first took office—now nearly ten years ago. I need hardly remind you that, back then, there were still important doctrinal differences between Argentina and the IMF—about the appropriate roles of the state and the private sector, the merits of economic liberalization, the need for fiscal equilibrium, and the virtues of deregulation. More than that, I recall that the term “Fund orthodoxy” had a negative connotation in Argentina in those days and that Fund missions provoked considerable public debate.

Today, there is no longer any doctrinal divide, and the arrival of IMF missions no longer causes a stir. Personally, I am delighted by this change of events. Why is the atmosphere so different today? Clearly, because of the fundamental changes that have taken place in recent years—in Argentina, Latin America, and the world. But it goes deeper than that. There is now considerable commonality of views throughout Latin America, and in much of the rest of the world, about what constitutes effective economic policy.

All of which is a typically long winded way of saying I get scared when I hear dogmatic talk about defense of the monetary order. Here’s German Chancellor Angela Merkel, on May 16, 2010:

“If the euro fails, not only the currency fails. Europe fails too, and the idea of European unification.”In a speech broadcast live on WDR television, Merkel said the crisis over the euro’s future was “not just any crisis, it is the strongest test Europe has faced since 1990, if not in the 53 years since the treaties of Rome.”“This test is existential — it must be passed. If it does not manage to (do that), the consequences for Europe and beyond are unforeseeable,” the conservative Christian Democrat said.