We can’t know what would have happened between the wars. But I have a feeling that we are about to find out why the Fed would ever have conducted itself so conservatively. And in a larger sense, we’re going to rediscover why policymakers ever thought it sensible to adhere to a ‘gold standard’. Put it another way. If it’s so clear to us why a gold standard is bad (Temin 1989) – and I agree that it is – why on earth did anyone sign up to it in the first place?

Are we, today, vastly enlightened compared to our forebears of merely eighty years ago, in a history of money that spans millennia? The truth is that in such a large and rare crisis as today’s, we look to the last crisis for answers. So did they. Their behaviour was forged from the lessons of their crucible. If our crucible is the Great Depression and its price deflation, their crucible was the abuse of unbacked money and its concomitant hyperinflation.

Hyperinflation genuinely occurred, and it was no mere sideshow in the global economy. It was burned into the collective sensibility of the interwar policy establishment. What today appear as freakish historical anecdotes were altogether real back then. It was more than the wheelbarrows of cash in the German, Austrian and Polish hyperinflations after the First World War. It was the collapse in a social compact between citizen and state. 1/

Our insistence on the ability of the monetary authority to counteract deflation might in fact move the money market from a state of mild deflation to very high inflation. A generalised deflation is not fanciful. Consider that Beijing is most likely to respond to weaknesses in the exporting sector in ways that exacerbate current downward price pressures. Should a severe downturn unfold there, perhaps linked to a crisis of their own, the authorities are likely to reach for the external sector as a pressure valve. This will take the form of administrative devaluation (e.g. issuing export rebates) and outright nominal currency devaluation through heavy fx intervention. The Chinese devaluation is essentially an outward shift in the supply curve. Add to this the need for many of China’s trade partners to follow the renminbi down. You can call it WTO-incompliant or ‘beggar thy neighbour’; there will be time to argue later.

Combine this with flight-to-safety flows from other currencies, and you get a strong dollar. Pretty hard to raise prices in those conditions. Yet there will be a still greater source of deflationary pressure: the flight to cash. A flight to cash is an increase in the demand for money. The deflationary impact of an increase in money demand takes two forms. First, the price level is an increasing function of the money supply and velocity (the number of transactions conducted with a unit of currency) and a decreasing function of total expenditure (for a given level of money supply and velocity). Money demand enters this picture through velocity: it is a declining function of money demand. Can the Fed expand the money supply as quickly as velocity is falling? Not only is it working against a falling rate of velocity, but also a decline in the money multiplier as the banking system contracts credit.

The danger is that the Fed’s attempts to boost the money supply become increasingly outrageous, to the point of shocking people out of their demand for paper dollars. We switch from an equilibrium of high money demand to one of low money demand. This sends velocity skyward, as agents transact the currency as quickly as they come into contact with it. To recap: The Fed is initially unable to sustain the price level through monetary expansion, partly because of the compressed money multiplier (banks refusing to lend) and partly because of the fall in velocity (people’s higher demand for real money balances). Resorting to increasingly helicopter-ish initiatives, it sparks a ‘naked emperor’ moment: The money market shifts from an equilibrium of falling prices and high money demand, to one of rising prices and low money demand.

Bear in mind the role of foreign buyers of US assets, principally US government debt. The lesser danger is that foreign official buyers of American debt stop supporting this market, perhaps through loss of faith in repayment without resort to the printing press. The real danger is that they do not merely withdraw support from the market, but directly undermine it (without malice, I hasten to add). These institutions own enough US government debt already to constitute competitors with the US Treasury itself in the event of disposal. In other words, the Treasury would compete with foreign central banks to sell the same asset into a finite pool of capital. Already the US Treasury market has a whiff of a Ponzi scheme about it: The US Government faces promised retirement and healthcare outlays exceeding plausible income by more than 50 trillion dollars in present value terms. Inflation won’t solve this, because these benefits were indexed to inflation following the last bout of fiscal irresponsibility in the 1970s (Kotlikoff and Burns 2005). 2/

Should such fanciful events unfold, it would be the failure of the most successful fiat money regime ever known. But it would not be the first fiat money failure, and not the first dollar-fiat closure. Where do you think the word ‘Greenback’ comes from? It was the currency issued directly by the US Treasury during the Civil War, unable to afford a metal standard. That era ended when a post-bellum United States went onto a gold standard in 1879.

The trouble with economic history – and perhaps financial history in particular – is knowing how far back to go. Perhaps the interwar hyperinflation is enough history to give us pause at the thought of a Bernanke’s eventual helicopter drop. But this post is about gold, and to understand its role in modern monetary history, you have to go back to the French Revolution. 3/ Facing extreme fiscal duress, the government of the National Assembly in 1789 issued a note backed by confiscated church property; these assignats were used to pay government expenses. They were “backed” in the sense that they could be redeemed at auction for the property; notes tendered at auction were subsequently destroyed.

The assignat became ‘fiat’, or un-backed, the moment the government printed it without regard to the auction scheme, impelled by a desperate situation in the nascent war of 1792. It naturally lost value. To compel money demand, the Jacobins threatened the guillotine for anyone not using the currency. By 1794, the urgency of the situation eased with France’s better fortunes in the war. Relieved of the compulsion to use the money, it was rejected in daily use. Velocity took off and France witnessed “the first classic hyperinflation in modern Europe” (Sargent and Velde 1995:476).

The lesson, of course, was distrust of fiat money. No government could ultimately escape the temptation to debase it; to finance its existence, its patrons and its adventures without public consent. This is precisely what the inflation tax is. For all its deficiencies, metal backing was plainly superior. This usually took the form of bimetallism (a gold and silver backing of the currency, with the metals exchangeable at the central bank at a fixed ratio). England was an outlier in operating a monometallic standard (gold), which became the universal standard by the time of America’s return to metallic backing in 1879.

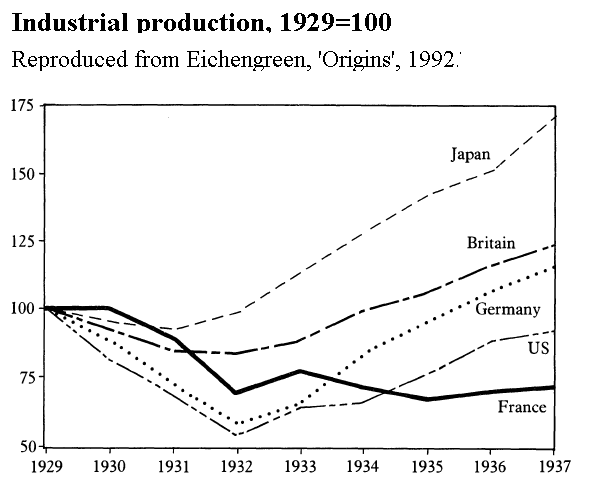

The gold standard did not abate with the First World War – it was merely suspended, as had often been the case in time of war. Indeed, America did not leave the gold standard during the war. The rest of the world resumed metal backing circa Britain’s resumption in 1925; by 1928, its international spread was more complete than even in the pre-war heyday. Conventional wisdom has it that the international gold standard ended a mere six years later, in a short window spanning, yet again, Britain’s 1931 devaluation.

With the benefit of the longest period of successful fiat money in history, we can see that the gold standard did not end in 1931. It merely evolved — as it had ever done, from the circulation of actual gold coin to the confiscation of such by the central bank for backing of note issue. The truth is that gold has been ‘monetized’ for millennia, on an official basis as recently as August 15, 1971, when the Untied States ended the US dollar’s convertibility into the substance. True, this latest manifestation was a distant relative of the ‘classical’ gold standard before World War One, insofar as conversion between dollars and gold was a privilege extended only to other central banks — US citizens having long since been relieved of the right even to hold the substance for other than numismatic purposes.

This is why I have written that gold’s future as a monetary asset should be taken seriously. Not because it would be advisable, but because gold has a force of inertia that demands respect: its monetisation goes back 2500 years, its abeyance 37.

Humbling though it may be, what attracts us to gold today is probably little changed from what attracted our distant ancestors. A specific set of qualities made it acceptable to them as a substitute for goods in barter, and so a store of value. It was universally distributed yet almost nowhere in very ready amounts. It was universally known and appealing for its inexplicable shine and rarity. It was, in the words of Carl Menger, eminently “salable” at market, and thus worthy of acceptance in lieu of barter. It’s difficult to peer back into the mists of time and confirm this; to know precisely why we ‘monetized’ gold. But for my money, Menger’s explanation is the best around. The definitive bits of his Economic Journal article are worth reproducing (Menger 1892):

The reason why the precious metals have become the generally current medium of exchange among here and there a nation prior to its appearance in history, and in the sequel among all peoples of advanced economic civilisation, is because their saleableness is far and away superior to that of all other commodities, and at the same time because they are found to be specially qualified for the concomitant and subsidiary functions of money.

There is no centre of population, which has not in the very beginnings of civilization come keenly to desire and eagerly to covet the precious metals, in primitive times for their utility and peculiar beauty as in themselves ornamental, subsequently as the choicest materials for plastic and architectural decoration, and especially for ornaments and vessels of every kind. In spite of their natural scarcity, they are well distributed geographically, and, in proportion to most other metals, are easy to extract and elaborate. Further, the ratio of the available quantity of the precious metals to the total requirement is so small, that the number of those whose need of them is unsupplied, or at least insufficiently supplied, together with the extent of this unsupplied need, is always relatively large-larger more or less than in the case of other more important, though more abundantly available, commodities. Again, the class of persons who wish to acquire the precious metals, is, by reason of the kind of wants which by these are satisfied, such as quite specially to include those members of the community who can most efficaciously barter; and thus the desire for the precious metals is as a rule more effective. Nevertheless the limits of the effective desire for the precious metals extend also to those strata of population who can less effectively barter, by reason of the great divisibility of the precious metals, and the enjoyment procured by the expenditure of even very small quantities of them in individual economy. Besides this there are, the wide limits in time and space of the saleableness of the precious metals; a consequence, on the one hand, of the almost unlimited distribution in space of the need of them, together with their low cost of transport as compared with their value, and, on the other hand, of their unlimited durability and the relatively slight cost of hoarding them. In no national economy which has advanced beyond the first stages of development are there any commodities, the saleableness of which is so little restricted in such a number of respects — personally, quantitatively, spatially, and temporally — as the precious metals. It cannot be doubted that, long before they had become the generally acknowledged media of exchange, they were, amongst very many peoples, meeting a positive and effective demand at all times and places, and practically in any quantity that found its way to market.

Hence arose a circumstance, which necessarily became of special import for their becoming money. For any one under those conditions, having any of the precious metals at his disposal, there was not only the reasonable prospect of his being able to convert them in all markets at any time and practically in all quantities, but also — and this is after all the criterion of saleableness — the prospect of converting them at prices corresponding at any time to the general economic situation, at economic prices. The proportionately strong, persistent, and omnipresent desire on the part of the most effective bargainers has gone farther to exclude prices of the moment, of emergency, of accident, in the case of the precious metals, than in the case of any other goods, whatever, especially since these, by reason of their costliness, durability, and easy preservation, had become the most popular vehicle for hoarding as well as the goods most highly favoured in commerce.

Under such circumstances it became the leading idea in the minds of the more intelligent bargainers, and then, as the situation came to be more generally understood, in the mind of everyone, that the stock of goods destined to be exchanged for other goods must in the first instance be laid out in precious metals, or must be converted into them, even if the agent in question did not directly need them, or had already supplied his wants in that direction. But in and by this function, the precious metals are already constituted generally current media of exchange. In other words, they hereby function as commodities for which every one seeks to exchange his market-goods, not, as a rule, in order to consumption but entirely because of their special saleableness, in the intention of exchanging them subsequently for other goods directly profitable to him. No accident, nor the consequence of state compulsion, nor voluntary convention of traders effected this. It was the just apprehending of their individual self-interest which brought it to pass, that all the more economically advanced nations accepted the precious metals as money as soon as a sufficient supply of them had been collected and introduced into commerce. The advance from less to more costly money-stuffs depends upon analogous causes.

This development was materially helped forward by the ratio of exchange between the precious metals and other commodities undergoing smaller fluctuations, more or less, than that existing between most other goods — a stability which is due to the peculiar circumstances attending the production, consumption, and exchange of the precious metals, and is thus connected with the so-called intrinsic grounds determining their exchange value. It constitutes yet another reason why each man, in the first instance (i.e. till he invests in goods directly useful to him), should lay in his available exchange-stock in precious metals, or convert it into the latter. Moreover the homogeneity of the precious metals, and the consequent facility with which they can serve as res fungibiles in relations of obligation, have led to forms of contract by which traffic has been rendered more easy; this too has materially promoted the saleableness of the precious metals, and thereby their adoption as money. Finally the precious metals, in consequence of the peculiarity of their colour, their ring, and partly also of their specific gravity, are with some practice not difficult to recognise, and through their taking a durable stamp can be easily controlled as to quality and weight; this too has materially contributed to raise their saleableness and to forward the adoption and diffusion of them as money.

My post has spoken of gold, where its monetisation came from, and how that monetisation has permeated history till practically the present. Yet the truth is that I’m no fan of an official link to gold. As someone whose main pursuit is studying the gold standard and the evolution of the international monetary system, I have come to the view that fiat money is one of the greatest inventions in history. It allows for the expansion of wealth through commerce and investment without need of painful price deflation. However, I’ve also come to accept that fiat money is like another great invention: fire. Like fire, it has the potential for immense good. Yet, when mishandled, it can wreak terrible havoc. A mishandling today – perhaps through ‘helicopter’ experiments – would not be the first fiat failure at the hands of an indebted sovereign unable to balance a largesse promised to its subjects with a means to pay for it.

1/ The ‘Austrian school’ would disagree: the state has no business monopolizing the creation of money, and arbitrarily dictating its price. Note-issuing private banks can do the same thing, so long as they hold gold to back a portion of their note issue.

2/ Ten percent of outstanding US debt in the hands of the public is inflation-indexed.

3/ Which validates the Chinese Communist Zhou Enlai, who contended in the second half of the twentieth century that it was still “too early” to assess the impact of the French Revolution.

Friedman, M. and Schwartz, A., A Monetary History of the United States (Princeton, 1963)

Kotlikoff, L. and Burns, S., The Coming Generational Storm: What You Need to Know about America’s Economic Future (Cambridge MA, 2005)

Menger, C., ‘On the origins of money’, Economic Journal 2 (1892).

Sargent, T. and Velde, F., “Macroeconomic features of the French Revolution”, Journal of Political Economy 103:3 (1995).

Temin, P., Lessons from the Great Depression (Cambridge MA, 1989).

{kind=link}