What would you say if more and more countries were being struck by the financial markets’ lack of confidence? You know. The bond markets are selling off. Depositors are leaving the banks. Not from caprice — from genuine worry. Worry over the high indebtedness of the private and/or sovereign sector. The poor growth outlook, thanks to a seriously overvalued currency. The serious people said: Stay in the currency at all costs. Push down domestic prices and wages. Give us an austerity budget to show you mean it. And that is precisely what they did:

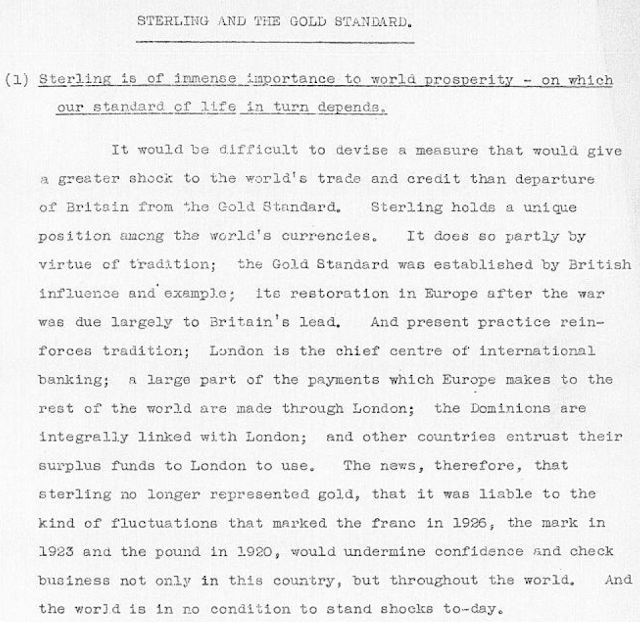

Cabinet Memo, British Prime Minister’s Office, Sept 1931

{kind=link}

Many decades later, the serious people reflected on that period, and pronounced something altogether different: austerity in defence of unrealistic monetary arrangements is masochism. For the synopsis of this view — and very much the standard-bearer — read Golden Fetters. Read just the introduction if you must. And to his credit, the author of this canonical work, Barry Eichengreen, is today the most honest of the serious people who say the euro-area members must defend the unrealistic monetary arrangements (i.e. stay in the euro). He is calling for a grand debt write-down for the affected euro-area sovereigns, and those yet to be affected. It’s honest and it’s intellectually coherent. Whether the euro-area non-leadership are equal to this challenge is another matter. They are not inferior, as policymakers go. They are just subject to the normal game-theoretic problems that beset us all.

Which is why I see Eichengreen’s proposal, meritorious though it is, as a non-starter. The exit route lay in devaluation. But please note: devaluation need only entail unilateral restructuring of debt if the sovereign comes out of the euro (which would entail forcibly re-denominating the debt). There is another way to devalue without upsetting debt contracts. Germany could come out of the euro. The rest of the euro-area would get the devaluation they desperately need.