It’s amazing to me how reluctant people are to prescribe euro-exit. Eichengreen stops well short; quite the contrary, he portrays such a move as disastrous. (The technical issues (ATMs, etc) and legal issues (cross-border debt contracts) are daunting, and the political cost is even worse: second-tier status in the EU if not outright expulsion.) If I read him right, Krugman describes euro-exit as disastrous though increasingly likely (its announcement would trigger “disastrous bank runs”). Last but not least, Domingo Cavallo — formerly Argentine finance minister — says the first lesson of Argentina’s 2001 crisis is that euro-exit is not the answer. Wow. Never mind that once Argentina devalued, real GDP growth shot to 7.5% and stayed there (barring the recent global downturn), whereas GDP was contracting in each of the four years leading up to the devaluation.

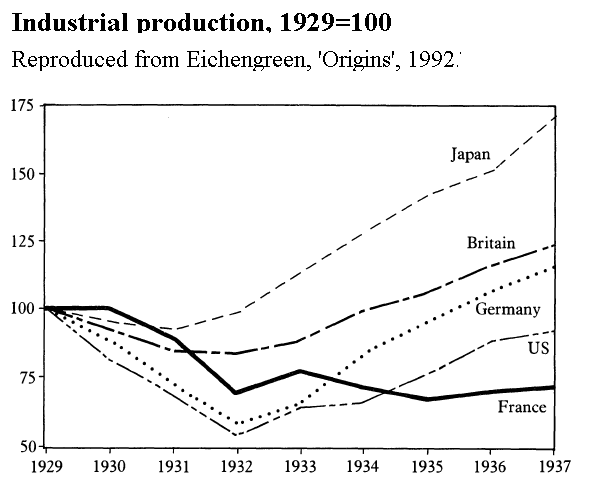

What’s striking about this widespread rejection of euro-exit is the re-writing of the lessons of the Great Depression — not least as detailed in Eichengreen’s masterpiece, Golden Fetters. The first to devalue (leave the gold standard) were the first to recover, almost without exception. Here’s the classic graph, where Japan is first out and France last:

Avoiding devaluation was committing the economy to long-term decline. Yet this is exactly what is prescribed for uncompetitive Europe today. Since default/restructuring won’t solve the long-term solvency concerns, the prescription is a deflationary grind — for the Greek, Ibero and Irish citizens (not to mention the longer-suffering Baltic ones). Wow. And this for a country already reporting the second-highest incidence of households with “real financial problems” and overdue on “many” credit commitments,

Efforts to keep Greece in the euro and the associated rhetoric are identical to those applied to countries on the verge of leaving the gold standard circa 1930-33. ‘Be more stringent.’ ‘Take your medicine’. ‘Roll back the credit structure’ and of course Mellon’s famous “Liquidate (everything)”. The French in particular pushed this view: the gold standard guaranteed global prosperity; defection undermined it. This stringent, orthodox prescription came from inflationary fears. And, as Eichengreen notes, “There is no little irony in the fact that inflation was the dominant fear in the depths of the Great Depression, when deflation was the real and present danger.” (Golden Fetters, 24).

How big is the technical hurdle to euro-exit? I suspect not as big as to justify the deflationary penury of staying in. The Bank of Greece is obviously a member of the eurosystem; but this also means that it keeps in touch with the distribution of euro notes both electronically and over the counter, as mandated by EU treaty.

Euro-exit also sounds like a much better outcome for the global economy and particularly the non-euro OECD. Would Britain and Turkey rather trade with a depressed Ireland/Club Med or a resurgent one? This is not a case of ‘money is neutral’ i.e. “Club Med will devalue one way or the other, domestic deflation or a new (and weaker) currency”. The former suggests years of stagnation and import compression, while the latter suggests at least a recovery in activity.

Devaluation (in these cases via currency defection) is not a guarantee of growth, but it makes it a lot more probable. That sure was the story in the interwar departures from the gold standard, where perhaps France was the main exception when it finally did devalue (1936). What the defecting countries will need is an upside-down “inflation stabilization program”. In these programmes, the government says, ‘We are going to stabilise (the freely falling) local currency against a (solid) foreign currency, and you (labour) are going to stop indexing wage settlement to a high rate of expected inflation.’ Instead, the government will have to say: ‘We are going to *stop* pegging the currency, and you (labour) are going to promise not to build-in higher wage claims.’

Much as I love using the euro, I would see its demise (at least in Club Med) as very bullish. What shocks me is how few people are explicit about this, and instead prescribe for Club Med today the same medicine that they criticize being given to our predecessors 80 years ago.