Referring to the argument that, Hey, we have a problem of too much debt. You can’t solve it by adding more debt. See Krugman versus the UK government on BBC Newsnight for a recent example (go to 39:00).

1. Reject the premise — that our problem is “too much debt”.

Our problem is not too much debt but too little! We are amidst a de-leveraging recession, a rare situation in which the private sector on a net basis is trying to improve its financial position. This might sound OK on an individual level but it’s a nightmare in aggregate. This is in fact why JM Keynes *invented* macroeconomics. He called it the “paradox of thrift”. One person’s (or firm’s or government’s) spending is another person’s (or firm’s or government’s) income. If you’re not spending, then I’m not earning. The vast majority of the money we would spend — if we wanted to spend it — is created through new lending by the financial system. But we’re doing the opposite right now: we’re trying on a net basis to pay down our debts. What this means is a shrinking in the money supply. So, reject the argument that the problem is “too much debt”. The problem is rather “too little debt.”

2. Compare the government not with a household but with a firm.

The market is offering you an interest rate of 3.27% on a 30-year term. Do you mean to say there are absolutely no projects which won’t pay better than a 3.27% rate of return? Honestly? For the government it’s especially straightforward — you don’t even need to “capture” those returns directly (as a firm would), you just need for those investments to enhance the economy’s (nominal) growth rate. Surely pouring money into educational infrastructure and people would pay a huge dividend for the economy’s growth, and this higher growth would come back to the government in the form of high tax revenues.

3. Analogously: You don’t have to balance your budget!

(And if you did seek to balance it, in effect you’re saying “Sorry, we just don’t see that there’s anything we can do that would make the economy work better.”) You just need to be sure that you can stabilize the ratio of debt to the economy in the medium term. Hell, you can even *grow* the amount of debt so long as the economy itself is growing! I’ll go one step further: you can grow the amount of debt outstanding even faster than you grow the economy! This is because, when the private sector comes back to life, you then do the opposite — grow debt slower than you grow the economy, because you know the private sector is doing the needed spending.

Un-learning the lessons of Great Depression (ad-infinitum)

This blog is full of lessons-unlearned since the Great Depression. Why so? Because, fortunately or not, I’ve spent a portion of the last several years working on the Great Depression from a monetary and policy perspective.

One of the interesting things about that period is the soul-searching it occasioned. This soul-searching is a good place to look for the policy lessons that were drawn from the experience (rightly or wrongly). Three of the key texts to me are Nurkse’s International Currency Experience (League of Nations, 1943), Lary’s The United States in the World Economy (US Commerce Department, 1943) and Haberler’s Prosperity and Depression (League of Nations, 1943).

Nurkse’s book in particular can be seen as a blueprint for what came at Bretton Woods, which laid down the international monetary order after the war. (Nurkse himself is an under-appreciated architect of that system.) One lesson hammered home in that book — and codified in the Bretton Woods arrangements — is the primacy of sovereign policymaking, specifically counter-cyclical policymaking. Nurkse wrote that it would no longer be possible for democratically elected governments to be expected to be indifferent to the employment and prosperity side-effects of their policies, in pursuit of some ‘grander’ aim — namely, exchange-rate stability. For this reason, the Bretton Woods system condoned controls on short-term capital.

What we are seeing today is the repudiation of that lesson. Eurozone policymakers are being asked to set aside the real-economy impact of austerity, in the name of monetary order. Isn’t this exactly what we (ie Western civilization) said we’d never do again?

One of the interesting things about that period is the soul-searching it occasioned. This soul-searching is a good place to look for the policy lessons that were drawn from the experience (rightly or wrongly). Three of the key texts to me are Nurkse’s International Currency Experience (League of Nations, 1943), Lary’s The United States in the World Economy (US Commerce Department, 1943) and Haberler’s Prosperity and Depression (League of Nations, 1943).

Nurkse’s book in particular can be seen as a blueprint for what came at Bretton Woods, which laid down the international monetary order after the war. (Nurkse himself is an under-appreciated architect of that system.) One lesson hammered home in that book — and codified in the Bretton Woods arrangements — is the primacy of sovereign policymaking, specifically counter-cyclical policymaking. Nurkse wrote that it would no longer be possible for democratically elected governments to be expected to be indifferent to the employment and prosperity side-effects of their policies, in pursuit of some ‘grander’ aim — namely, exchange-rate stability. For this reason, the Bretton Woods system condoned controls on short-term capital.

What we are seeing today is the repudiation of that lesson. Eurozone policymakers are being asked to set aside the real-economy impact of austerity, in the name of monetary order. Isn’t this exactly what we (ie Western civilization) said we’d never do again?

Abenomics

Abenomics (noun): The use of macro policy to stimulate the economy. See also “Keynesianism”.

Japan’s newfound enthusiasm for macro policy is going to provide a helluva interesting real-life test of the competing notions over whether OECD governments are doing too much or too little to tackle anaemic growth rates.

My guess is that the austerians will have to come up with reasons why Japan’s muscular and highly interventionist policies aren’t sparking hyperinflation, a yen collapse or some other cataclysm.

But from a strictly positive point of view, it will make for an interesting case study. Here we have a government that is basically saying, We’re going to debase our currency. Yet it has too much credibility as a state, a society, to be credible in this threat.

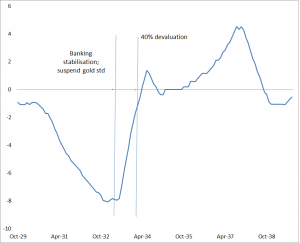

Here’s an example of turning deflation into inflation (US CPI excl food, source: NBER Macrohistory database):

Most of the time-series from the US macro situation in the 1930s tell me the single most important policy action was devaluing the dollar. Why? Because it shifted people’s expectations, from deflation to inflation, and thereby eased real interest rates.

Most of the time-series from the US macro situation in the 1930s tell me the single most important policy action was devaluing the dollar. Why? Because it shifted people’s expectations, from deflation to inflation, and thereby eased real interest rates.

In order to ensure that devaluation, the US had to commit to buy unlimited quantities of the numeraire unit — i.e. gold. In today’s world, Japan would have to commit to buying unlimited US dollars.

Japan’s newfound enthusiasm for macro policy is going to provide a helluva interesting real-life test of the competing notions over whether OECD governments are doing too much or too little to tackle anaemic growth rates.

My guess is that the austerians will have to come up with reasons why Japan’s muscular and highly interventionist policies aren’t sparking hyperinflation, a yen collapse or some other cataclysm.

But from a strictly positive point of view, it will make for an interesting case study. Here we have a government that is basically saying, We’re going to debase our currency. Yet it has too much credibility as a state, a society, to be credible in this threat.

Here’s an example of turning deflation into inflation (US CPI excl food, source: NBER Macrohistory database):

Most of the time-series from the US macro situation in the 1930s tell me the single most important policy action was devaluing the dollar. Why? Because it shifted people’s expectations, from deflation to inflation, and thereby eased real interest rates.

Most of the time-series from the US macro situation in the 1930s tell me the single most important policy action was devaluing the dollar. Why? Because it shifted people’s expectations, from deflation to inflation, and thereby eased real interest rates. In order to ensure that devaluation, the US had to commit to buy unlimited quantities of the numeraire unit — i.e. gold. In today’s world, Japan would have to commit to buying unlimited US dollars.

A macroeconomic union

The euro’s main political effect is to drive a wedge through the EU, something not yet fully understood by the bloc’s policy establishment. The vast majority of insiders still treat it as a regulatory organisation at its heart, rather than as a macroeconomic union.Wolfgang Münchau in today’s FT

Props to Münchau for putting so succinctly a sentiment I’ve had for a while. I’ve had a niggling feeling that the damage being done by the euro-effort is not just to the euro-members but to the EU.

How ironic that the guardians of the euro (and self-declared guardians of Europe) might dissemble the very body they claim to be protecting. I personally don’t think there can be an EU and a euro-zone with non-perfectly-overlapping memberships.

Pathways out of the euro-zone crisis

Lecture presented to the Georgetown University Graduate Program in International Management (Oxford, August 2012).

Slides (pdf)

Audio (mp3)

Audio TOC:

0:00 Introduction, Plan of the talk

1:00 Real exchange rate

4:10 Purchasing Power Parity

6:05 East Asia crisis

10:37 Hong Kong is the exception

14:20 Financial globalization

16:45 Internal devaluation in Argentina

20:00 Greece

23:10 Pathways out of the crisis

25:10 De-globalization in Europe?

26:41 Monetary trilemma

28:38 History Lesson: The Great Depression

35:43 Beware dogmas

37:12 Q: How can you have capital controls without a black market?

39:24 Gresham’s Law: ‘bad money chases out good’

41:16 Q: How effective is devaluation if you don’t have a strong export market?

44:00 How can Greek democracy produce the ‘right’ policy?

46:44 Q: Is there a role for the private sector in this crisis?

49:25 Krugman solution — ‘creditor adjustment’ — disastrous precedents

54:25 Q: Can China do something to help?

56:10 Q: How can the IMF get it so wrong?

Crisis devaluations

Still thinking about a euro-area breakup. The question for this project is: For a given current account deficit and prior real appreciation, how big is the devaluation?

The dataset contain 36 devaluation episodes, all of which featured a minimum 15% nominal depreciation over six months less-than-fully offset by inflation (i.e. a real depreciation). They are all pre-2008 so do not include the flight-to-liquidity event associated with the Lehman Brothers collapse.

These events struck developed as well as developing economies; the 1990s capital-account crises are all there. As it happens, real per capita GDP (log terms) makes no difference to the results.

In the language of econometrics, what I’m doing is estimating the following equation:

devaluation = constant + real appreciation + ca deficit + per-capita GDP in constant PPP dollars

where all terms are logs or log-change except ca deficit, which is in percent.

Here are the descriptive statistics for the variables:

The dataset contain 36 devaluation episodes, all of which featured a minimum 15% nominal depreciation over six months less-than-fully offset by inflation (i.e. a real depreciation). They are all pre-2008 so do not include the flight-to-liquidity event associated with the Lehman Brothers collapse.

These events struck developed as well as developing economies; the 1990s capital-account crises are all there. As it happens, real per capita GDP (log terms) makes no difference to the results.

In the language of econometrics, what I’m doing is estimating the following equation:

devaluation = constant + real appreciation + ca deficit + per-capita GDP in constant PPP dollars

where all terms are logs or log-change except ca deficit, which is in percent.

Here are the descriptive statistics for the variables:

| nominal depreciation | prior real appreciation | prior ca deficit | gdp per cap (2005 PPP$) | |

| mean | 0.37 | 0.21 | -2.88 | 13,696 |

| sd | 0.28 | 0.27 | 3.32 | 9,815 |

| min | 0.16 | 0.00 | -9.73 | 793 |

| max | 1.30 | 1.52 | 3.97 | 34,233 |

| N | 36.00 | 36.00 | 36.00 | 36.00 |

Thinking about a eurozone breakup

This project draws on post-Bretton Woods history of large-scale currency moves. Each observation marks the date at which the currency collapsed or went from slow fall to freefall. The penultimate column is the change in the nominal exchange rate over the following months. The final column is the cpi inflation rate from the breakup plus 12 months. To qualify as an event, the exchange rate must drop a minimum of 20% over six months. The events of interest are those which were not offset by inflation; we’re interested in big real depreciations.

| ccode | country | date | ncusdep | precp~12 | deval | tempcpi |

| 5 | Argentina | 2002m1 | .9991032 | 117.7919 | -69.49303 | .3336353 |

| 7 | Australia | 1989m1 | 1.126888 | 83.76093 | -13.3987 | .0779939 |

| 20 | Brazil | 2001m2 | 2.035467 | 74.89955 | -13.3032 | .0914023 |

| 29 | China | 1984m8 | 2.4196 | 231.7714 | -17.04608 | -.2707708 |

| 29 | China | 1989m11 | 3.7314 | 129.1318 | -28.72479 | .043798 |

| 29 | China | 1993m12 | 5.8145 | 79.85056 | -31.32102 | .2271347 |

| 30 | Colombia | 2002m6 | 2398.82 | 67.52859 | -14.85454 | .0696445 |

| 54 | Greece | 1991m2 | 163.3496 | 156.8637 | -13.58084 | .1576862 |

| 63 | Indonesia | 1986m8 | 1132.292 | 553.7112 | -30.93792 | .0881588 |

| 63 | Indonesia | 1997m6 | 2430.583 | 61.029 | -83.66028 | .3670013 |

| 67 | Israel | 1988m11 | 1.5855 | 190.0603 | -19.25134 | .1821845 |

| 70 | Japan | 1995m7 | 88.38814 | 81.24142 | -17.72081 | .0039606 |

| 75 | South Korea | 1997m9 | 914.4 | 83.43518 | -34.26312 | .0664587 |

| 89 | Malaysia | 1997m7 | 2.639 | 77.51146 | -36.33294 | .0423975 |

| 91 | Malta | 1992m9 | .3009864 | 102.0785 | -20.84933 | .0397878 |

| 94 | Mexico | 1982m1 | .02654 | 8504.664 | -82.14598 | .7421452 |

| 94 | Mexico | 1985m6 | .245 | 1979.982 | -61.62881 | .6052652 |

| 94 | Mexico | 1994m11 | 3.4386 | 167.5194 | -54.43571 | .3951592 |

| 104 | New Zealand | 1984m6 | 1.577287 | 67.23439 | -23.6593 | .1537352 |

| 115 | Philippines | 1983m5 | 10.083 | 322.3331 | -27.98885 | .2621531 |

| 115 | Philippines | 1997m6 | 26.384 | 107.2274 | -37.31676 | .0801048 |

| 116 | Poland | 1991m4 | .9500034 | 221.4435 | -30.80303 | .4270055 |

| 117 | Portugal | 1992m9 | 125.5 | 107.8306 | -24.94901 | .062161 |

| 121 | Russia | 1998m7 | 6.238 | 125.933 | -74.21249 | .4046242 |

| 129 | Slovenia | 1995m7 | 112.8545 | 126.0007 | -14.46881 | .0869267 |

| 131 | South Africa | 1996m1 | 3.6523 | 160.2984 | -19.96012 | .0862052 |

| 131 | South Africa | 2001m8 | 8.3963 | 68.81133 | -21.01243 | .0852447 |

| 132 | Spain | 1992m8 | 91.51575 | 111.5168 | -31.71966 | .0494118 |

| 136 | Sweden | 1982m9 | 6.28 | 92.05548 | -19.59027 | .090193 |

| 136 | Sweden | 1992m9 | 5.304 | 88.97937 | -34.35644 | .0413332 |

| 137 | Switzerland | 1987m12 | 1.2715 | 69.04295 | -15.3462 | .0187459 |

| 137 | Switzerland | 1991m1 | 1.258 | 72.56998 | -11.96641 | .0475683 |

| 137 | Switzerland | 1992m9 | 1.2372 | 72.46855 | -13.54298 | .0341811 |

| 142 | Thailand | 1997m6 | 24.69568 | 75.08898 | -41.46547 | .1005292 |

| 146 | Turkey | 1991m1 | .0030449 | 27510.29 | -44.55163 | .5306886 |

| 146 | Turkey | 2001m1 | .6807995 | 114.1013 | -48.58105 | .4906485 |

| 151 | UK | 1981m1 | .420964 | 122.173 | -20.71143 | .1079772 |

| 151 | UK | 1984m8 | .7634753 | 90.58382 | 6.619332 | .0514967 |

| 151 | UK | 1992m8 | .5039052 | 96.53842 | -25.00378 | .0171313 |

Re-creating the Great Depression — interview with Amber Murrey (mp3)

Podcast (7 minutes)

The euro and the Great Depression – conference presentation slides (PDF)

Here are my slides (pdf) from the talk I gave at the euro-crisis conference in Bayreuth, Germany in January 2012.

And here are some reflections upon that conference:

1) Heads in the sand

Most people said “The current route (internal devaluation) isn’t working” and also “nothing else is possible — especially external devaluation”.

2) Key disagreement

The key contention was between those who believed in a Keynesian / Eichengreen interpretation and those who didn’t. Two interesting things about this: (i.) The Keynesians think that by staying in the euro, illiberal outcomes will be courted (i.e. trade barriers, capital controls), and (ii.) The Keynesians came exclusively from non-Eurozone countries: UK, Switz and Sweden. The people most fiercely against the Keynesian ideas were from Germany and Greece.

3) Reflections

Interesting that EZ countries (Greece) have not yet suffered a “sudden stop” in the way that East Asia did upon its crisis or the indeed the Europeans did in their 1931 crisis. Instead, official financing is still bridging the gap. Which is analogous to the Argentina story, in the sense that IMF money bridged things over until that money was rejected/withdrawn.

“Liberalism”. I in particularly urged people to consider that by forcing countries to stay in the euro (or indeed “helping” them to stay in the euro), the result might be highly illiberal as countries are forced to adopt capital controls and/or trade barriers to countenance severe currency overvaluation with domestic reflation. After all, the polities are not going to stand recession forever. An interesting counterpoint was made by a Cyprus delegate at the conference: He thought that by allowing Greece (or Italy etc) to devalue, you take the pressure off of them to reform. In other words, only by staying in the euro to keep up the pressure on these government to reform and liberalise. Very interesting stuff either way. My own view is you have to do both: Keep up the pressure for reform, but do so in a growth environment, which absolutely requires an external devaluation.

Internal devaluation versus external devaluation. We had presentations from both Latvia and Estonia on their (generally successful) internal devaluations. Essentially, both presenters said: “Yes, we devalued internally, but you probably can’t.” Because only these countries have the motivation to succeed (ex-Soviet) and the lack of labour rigidities.